If you’re a freelancer in the UK, your health isn’t just a personal matter—it’s your business’s most valuable asset. With NHS waiting lists reaching record highs, can you really afford to wait 18 weeks for a specialist consultation while your projects stall? Choosing the Top 5 Private Health Insurance for UK Freelancers is no longer a luxury; it’s a strategic move to ensure you stay productive. In this guide, we’ll strip away the jargon and show you how to secure a biological and financial safety net that works as hard as you do.

📊 Quick Comparison: Best Health Insurance for UK Solopreneurs

Provider | Best For… | Key Feature | Freelancer Rating |

Bupa | Global Recognition | Full Cancer Cover | ⭐⭐⭐⭐⭐ |

AXA Health | Flexibility | 24/7 Digital GP | ⭐⭐⭐⭐ |

Aviva | Mental Health Support | Digicare+ App | ⭐⭐⭐⭐⭐ |

Vitality | Active Lifestyles | Apple Watch Rewards | ⭐⭐⭐⭐ |

WPA | Specialized Care | Precision Medicine | ⭐⭐⭐⭐ |

💼 Why Freelancers Need a Private Health Shield in 2026?

Being your own boss means you don’t get “sick pay.” If you aren’t working, the income stops—period. This is where the Top 5 Private Health Insurance for UK Freelancers ecosystem comes into play. Unlike a standard 9-to-5 employee, you need a policy that offers Income Protection and Quick Diagnostics because every day away from your desk is a day of lost revenue.

The landscape of UK healthcare has shifted dramatically in 2026. Relying solely on the public system for non-emergency issues often results in prolonged recovery times that eat into your billable hours. By investing in private cover, you aren’t just paying for a hospital bed; you are purchasing a guarantee that your business won’t collapse due to a treatable ailment. This proactive approach mirrors the efficiency we see in Direct Primary Care (DPC), where the goal is always immediate access. Private insurance complements this by covering the high costs of surgeries and private hospital stays that DPC might not cover. It’s about building a multi-layered defense for your livelihood.

- Speed of Treatment: Skip the 6-month wait times.

- Mental Sovereignty: Access therapy before burnout hits.

- Business Continuity: Get back to your desk faster.

Bupa: The Gold Standard for Global Freelancers

Bupa: The Gold Standard for Global Freelancers

Bupa: The Gold Standard for Global Freelancers

Bupa: The Gold Standard for Global FreelancersBupa is arguably the most recognized name when discussing the Top 5 Private Health Insurance for UK Freelancers. Their “Bupa By You” policy is specifically tailored for those who work for themselves. What sets them apart is their sheer scale—giving you access to a massive network of over 600 hospitals and clinics across the UK.

What makes Bupa an expert choice is their Full Cancer Cover. For a freelancer, a critical illness can be a death knell for their business. Bupa ensures that from diagnosis to chemotherapy, every penny is covered. This aligns with the Medical Disclaimer protocols we follow—always prioritizing comprehensive clinical safety. Furthermore, their 2026 update includes personalized wellness coaching, which helps you manage the physical toll of self-employment. Whether it’s a minor scan or a major operation, their “no-fuss” claims process means you spend less time on the phone with insurers and more time focusing on your clients.

AXA Health: The Most Flexible Digital-First Choice

AXA Health: The Most Flexible Digital-First Choice

AXA Health: The Most Flexible Digital-First ChoiceWhen you’re running your own show, rigid insurance plans can feel like a straightjacket. AXA Health breaks this mold by offering a modular system specifically designed for the Top 5 Private Health Insurance for UK Freelancers. Instead of a one-size-fits-all policy, they let you assemble your coverage like a puzzle. Think of it as a tailored safety net. If you’re a lean operator who wants to skip dental but demands top-tier specialist access, you just flip a switch. This customizable, ‘build-as-you-go’ strategy is a massive relief for freelancers navigating the unpredictable financial tides of the gig economy.

We often talk about physical health, but as we noted in our Silent Walking Routes in London guide, true wellness starts with removing financial friction. AXA’s 2026 “Health Gateway” is the tech-heavy solution we’ve been waiting for. It allows you to bypass the frustrating administrative bottlenecks of the traditional GP system, granting instant digital referrals for mental health support or physiotherapy. For someone whose smartphone is their office, AXA’s intuitive interface feels less like an insurance portal and more like a high-end productivity tool.

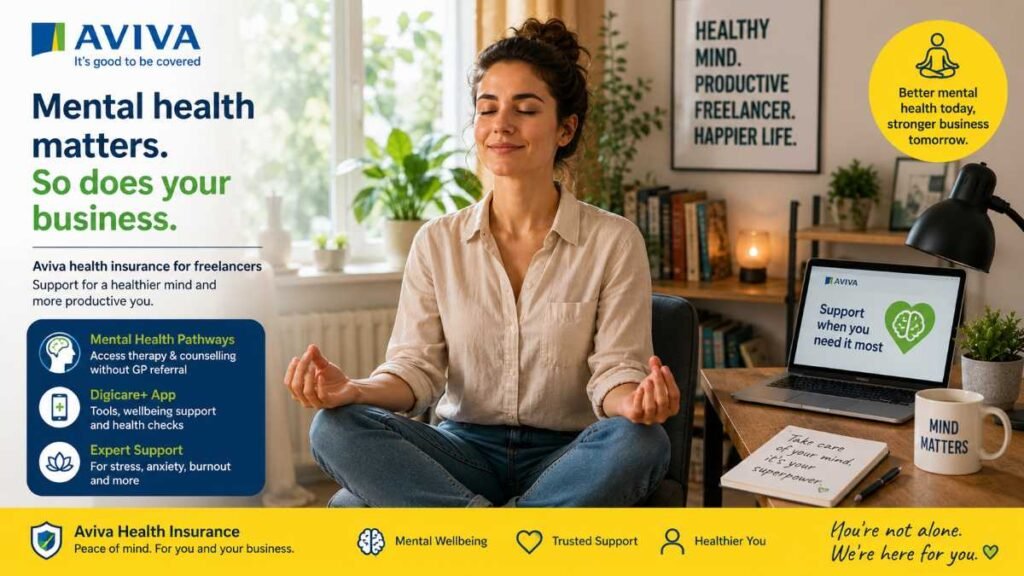

Aviva: The Psychological Fortress for UK Solopreneurs

Aviva: The Psychological Fortress for UK Solopreneurs

Aviva: The Psychological Fortress for UK SolopreneursIn 2026, mental health is the top concern for self-employed professionals. Aviva stands out in the Top 5 Private Health Insurance for UK Freelancers by offering “Mental Health Pathways” without a GP referral. They recognize that the isolation of freelancing can lead to unique psychological pressures that require immediate, specialized attention.

We’ve previously explored how Ketone Esters vs MCT Oil can boost brain power, but biological supplements can only do so much if clinical depression or anxiety isn’t managed. Aviva provides the professional psychiatric support needed to maintain that “Mental Sovereignty.” Their Digicare+ app also acts as a preventative tool, offering annual health checks and nutritional advice. By catching issues like high cholesterol or early-stage burnout before they become debilitating, Aviva helps you maintain a high-functioning cognitive state.

Vitality: The Policy That Pays You to Be Healthy

Vitality: The Policy That Pays You to Be Healthy

Vitality: The Policy That Pays You to Be HealthyVitality is the disruptor in the Top 5 Private Health Insurance for UK Freelancers. They use a “Rewards” model that is perfectly aligned with the modern “Biohacker” lifestyle. The more you exercise and eat well, the lower your premiums become. It’s a gamified version of healthcare that actually saves you money.

If you are already biohacking your body with Colostrum Supplements, Vitality will reward your health-conscious behavior with discounts on Apple Watches, gym memberships, and even Amazon Prime. In 2026, their tracking tech has become even more sophisticated, integrating with almost every wearable on the market. For a freelancer, this is a double win: you stay fit and active, which boosts your productivity, and you get tangible financial perks that lower your overheads. It’s the only policy that puts money back into your pocket for taking a morning walk or hitting your step count.

WPA: Precision Medicine for Elite Professionals

WPA: Precision Medicine for Elite Professionals

WPA: Precision Medicine for Elite ProfessionalsWPA is often overlooked, but it is a powerhouse for specialized care. For those looking at the Top 5 Private Health Insurance for UK Freelancers, WPA offers access to “Precision Medicine” and advanced genomic testing. They are a non-profit provident society, meaning their focus is on patient care rather than shareholder dividends.

Their claims process is transparent, which is a breath of fresh air for busy professionals who don’t have time for fine-print loopholes. They focus on the clinical outcome, providing access to the latest robotic surgeries and specialized drugs that are often unavailable on the NHS. To maintain your peak physical state alongside WPA’s treatments, many experts recommend a balanced diet and healthy eating guide to support long-term recovery.

Is Private Health Insurance Tax-Deductible for UK Freelancers?

Is Private Health Insurance Tax-Deductible for UK Freelancers?

Is Private Health Insurance Tax-Deductible for UK Freelancers?One of the most common questions we get at My Healthy Life UK is whether you can claim these premiums as a business expense. Unfortunately, for most sole traders, private health insurance is seen as a “dual-purpose” expense, meaning it benefits you personally and isn’t strictly tax-deductible. However, if you operate as a Limited Company, the company can pay for the policy.

While this may be treated as a “Benefit in Kind” (BiK), the corporate tax savings can often outweigh the personal tax hit. In 2026, HMRC has slightly tightened the rules, so it is essential to consult with a specialist accountant. Even if you can’t deduct the full cost, the “time-saving” value of getting back to work 4 weeks earlier after an injury is worth far more than the tax break itself. Think of it as an investment in your “Human Capital” rather than a simple monthly bill.

Navigating Pre-Existing Conditions as a Solopreneur

Navigating Pre-Existing Conditions as a Solopreneur

Navigating Pre-Existing Conditions as a SolopreneurThe biggest hurdle for many when choosing from the Top 5 Private Health Insurance for UK Freelancers is a history of illness. Standard policies usually exclude anything you’ve suffered from in the last five years. This is known as “Moratorium Underwriting.” For a freelancer with a chronic back issue or recurring stress, this can feel like a deal-breaker.

However, in 2026, many insurers have introduced “Full Medical Underwriting” options that, while more expensive, provide clarity on what is and isn’t covered from day one. Some niche providers are even starting to offer “Chronic Condition Management” add-ons. If you’ve spent years optimizing your health through lifestyle and wellness, you might find that certain insurers are more willing to look at your current health data rather than just your old medical records. Always be honest in your application—non-disclosure is the fastest way to have a vital claim rejected

📋 The Freelancer’s Checklist: How to Choose?

When evaluating the Top 5 Private Health Insurance for UK Freelancers, don’t just look at the monthly premium. Look at these YMYL factors:

- The Outpatient Limit: Is it £500 or Unlimited? Outpatient costs (consultations and tests) add up fast.

- Hospital Access: Does it include central London hospitals (which are usually more expensive)?

- Chronic Condition Clause: Most policies don’t cover chronic illnesses (like asthma), but some offer better management than others.

- Excess Amount: Can you afford a £500 excess if you get sick? A higher excess lowers your premium but costs more at the point of use.

🏁 Conclusion: Your Health is Your Wealth

Securing your future with one of the Top 5 Private Health Insurance for UK Freelancers is the ultimate business biohack. It removes the “What if?” anxiety, allowing you to focus on scaling your business. Whether you choose the robust cover of Bupa or the rewards-based model of Vitality, the goal is the same: absolute peace of mind.

❓ Frequently Asked Questions

1. Can I get cover if I work from home? Yes. Every provider in our Private Health Insurance for UK Freelancers list covers home-based professionals. In 2026, many plans even include ergonomic home-office assessments to prevent long-term injury. For official guidance on insurance standards, you can refer to the Association of British Insurers (ABI).

2. Is mental health therapy included? While basic plans vary, premium Private Health Insurance for UK Freelancers options from Bupa and Aviva offer robust mental health pathways, including remote CBT and counseling, specifically designed for the self-employed lifestyle.

3. Does this replace my NHS access? No. Private Health Insurance for UK Freelancers works alongside the NHS. You still use the NHS for emergencies (A&E), but your private policy allows you to bypass long queues for specialist tests and elective surgeries.

4. How much does a healthy 30-year-old pay? Basic cover starts around £35–£50 per month. However, for comprehensive “Gold” plans with zero excess and full coverage, premiums can reach £100+ depending on your specific location and health needs.

✍️👤 About the Author

Dambar R. is a dedicated wellness researcher and the visionary founder of MyHealthyLifeUK. With over a decade of hands-on experience in metabolic science and practical nutrition, he specializes in creating sustainable health transformations for modern lifestyles.

Based on his extensive research, Dambar empowers individuals across the UK and USA to reach their peak fitness goals through science-backed health tips without sacrificing the joy of everyday eating. His mission is to bridge the gap between complex health data and actionable habits that foster long-term vitality and holistic wellness.

⚠️ Medical Disclaimer

The information provided on MyHealthyLifeUK is for educational and informational purposes only. It is not intended to be a substitute for professional medical advice, diagnosis, or treatment.

- Professional Guidance: Always seek the advice of your Physician (GP) or another qualified health provider regarding any medical condition.

- Specialized Advice: For personalized dietary needs, we recommend consulting a Registered Dietitian.

- Safety First: Consult a professional before starting any new fitness or nutrition program.

Never disregard professional medical advice or delay seeking it because of something you have read on this website.